Analysis shared exclusively with TBR Football sheds new light on ENIC’s valuation of Tottenham Hotspur amid scepticism about the Lewis family’s statement that the club is ‘not for sale’.

Daniel Levy spent almost exactly a quarter of a century at Tottenham. In that time, the club’s value increased by roughly £3.20 every time the former investment banker’s heart beat. Not bad, especially for a chairman who was initially appointed only on an interim basis.

Joe Lewis’ ENIC bought into Spurs in 2000, with their initial deal valuing the North London club at around £80m.

Ostensibly, the Premier League football had just entered its champagne era.

After selling itself to the world, the division’s TV deal was about to top £1bn for the first time, global capital was flooding into the sport, and new media had made footballers internationally marketable.

But long after he had exited the club for good, former Tottenham owner Alan Sugar memorably said that Premier League money was more like “prune juice” than champagne: in one end, out of the other.

For every pound that clubs earned in booming media, matchday and commercial revenue, they spent more on player wages, transfers and agents’ fees, pouring water in a leaky bucket.

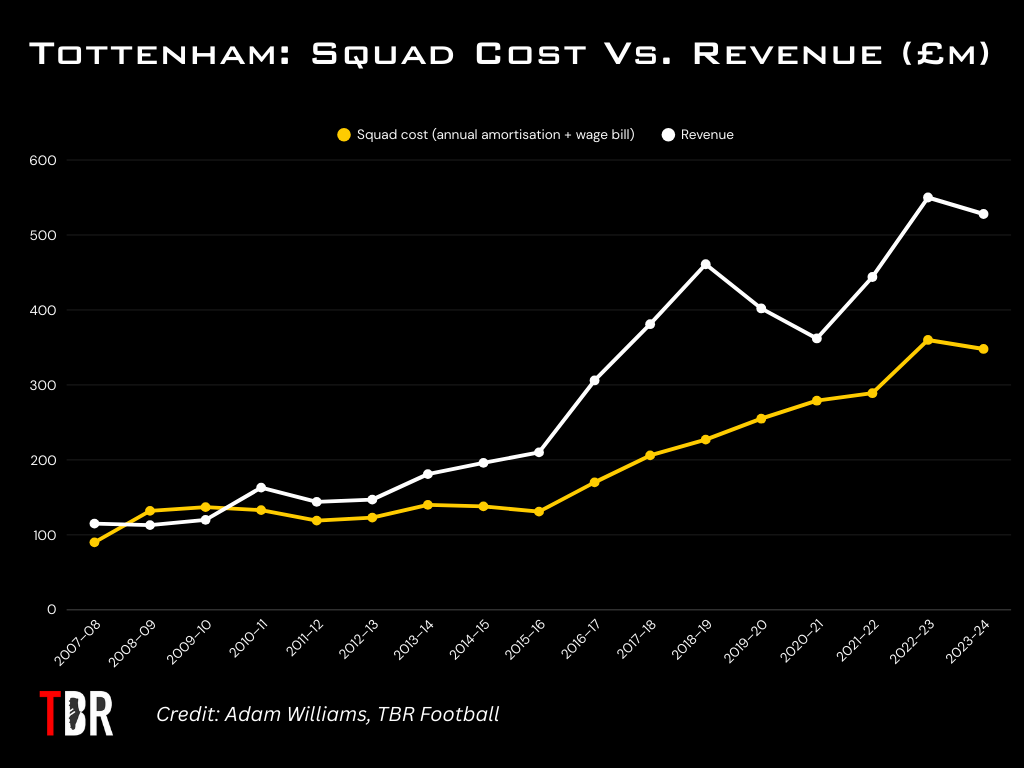

Spurs, however, were the exception. Until recently, they have been almost entirely financially self-sufficient, with no reason for their executives to fly out to the Bahamas – the tax haven from where the Lewis family operates – with cap in hand.

The Tottenham Hotspur Stadium, funded by cheap debt, has made the club a global brand by brute force.

Spurs’ annual commercial income (£255m at the last count) is higher than the total revenues of all but five English clubs. With 15 general admission and seven premium tiers of tickets, Spurs’ uber-sophisticated matchday strategy will generate in excess of £150m this season. TV and streaming continues to bring home the bacon too.

That means that, even in a fallow year, Spurs are dead certs to be in the top-10 revenue generators in world football.

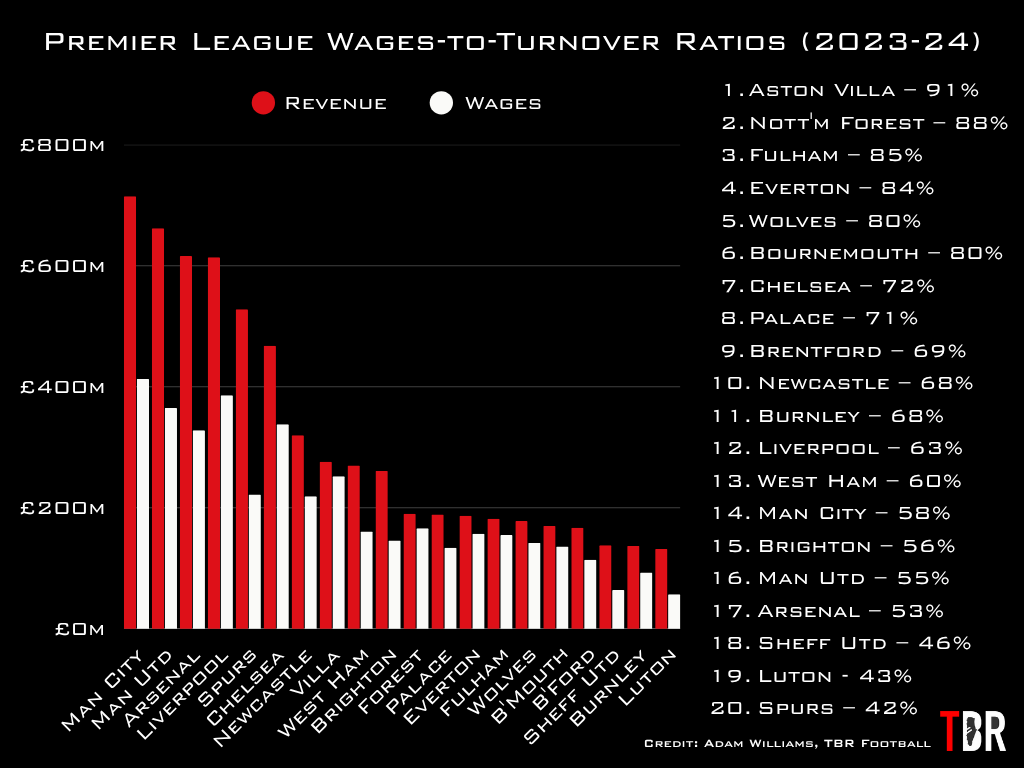

Meanwhile, Levy’s almost religious devotion to cost control – yes, Spurs did indeed have the Premier League’s lowest wages-to-turnover ratio at around 42 per cent in the last financial year – has historically made him the perfect administrator for ENIC.

EBITDA is high, interest repayments low, and capital appreciation relentless.

But Tottenham fans, whose protests grew louder than ever last season, have been keen to point out that it’s the green bit between the four corner flags that really matters, not spreadsheets and ticker tape.

Last season, they somehow elbowed their way into the Champions League – where they began their 2025-26 campaign with 1-0 victory over Villareal last night – but finished 17th in the league.

It was one of the strangest seasons in their history and, despite it ending in Europa League quasi-glory, Levy has been encouraged to resign off the back of it. But the 63-year-old leaves behind a club which, at its molten core, has everything needed to become one of the world’s best.

Levy’s consigliere Donna-Maria Cullen is gone too, and CEO Vinai Venkatesham is now steering the ship alongside non-executive chairman Peter Charrington.

No sooner had the Levy regime been disbanded, the club clarified that it had rejected two takeover offers from Amanda Staveley’s PCP International Finance and a consortium led by Dr Roger Kennedy and Wing-Fai Ng.

But neither a minority investment deal nor a takeover of ENIC, not the club, have been ruled out. And, unlike with the two offers for outright control to date, Spurs would be under no obligation to immediately disclose those plans under the UK Takeover Code.

The issue of price remains, however. Levy wanted £3.75bn and had enlisted the Rothschild bank to help him smoke out investors at that price point, to no avail.

So how much are Tottenham really worth? A new study has an intriguing take.

Exclusive: Tottenham valued at £3bn, trumping Liverpool, Man United and more

Beauty is in the eye of the beholder and ‘value’ is ultimately defined by the whims of the market.

But every year, the likes of Forbes, KPMG’s Football Benchmark, Sportico and others rank football clubs by value. And every year, the graph trends up and to the right.

| Rank | Club | Value | One-year change |

| 1 | Real Madrid | £5.53bn | 2% |

| 2 | Manchester United | £5.41bn | 1% |

| 3 | Barcelona | £4.63bn | 1% |

| 4 | Liverpool | £4.43bn | 1% |

| 5 | Manchester City | £4.35bn | 4% |

| 6 | Bayern Munich | £4.18bn | 2% |

| 7 | Paris Saint-Germain | £3.77bn | 5% |

| 8 | Arsenal | £2.79bn | 31% |

| 9 | Tottenham Hotspur | £2.71bn | 3% |

| 10 | Chelsea | £2.67bn | 4% |

Spurs are typically valued at between £2.5bn and £3bn by most assessors, which tends to be comfortably lower than the likes of Liverpool, Manchester City, Manchester United and European giants like Real Madrid, Paris Saint-Germain and Bayern Munich.

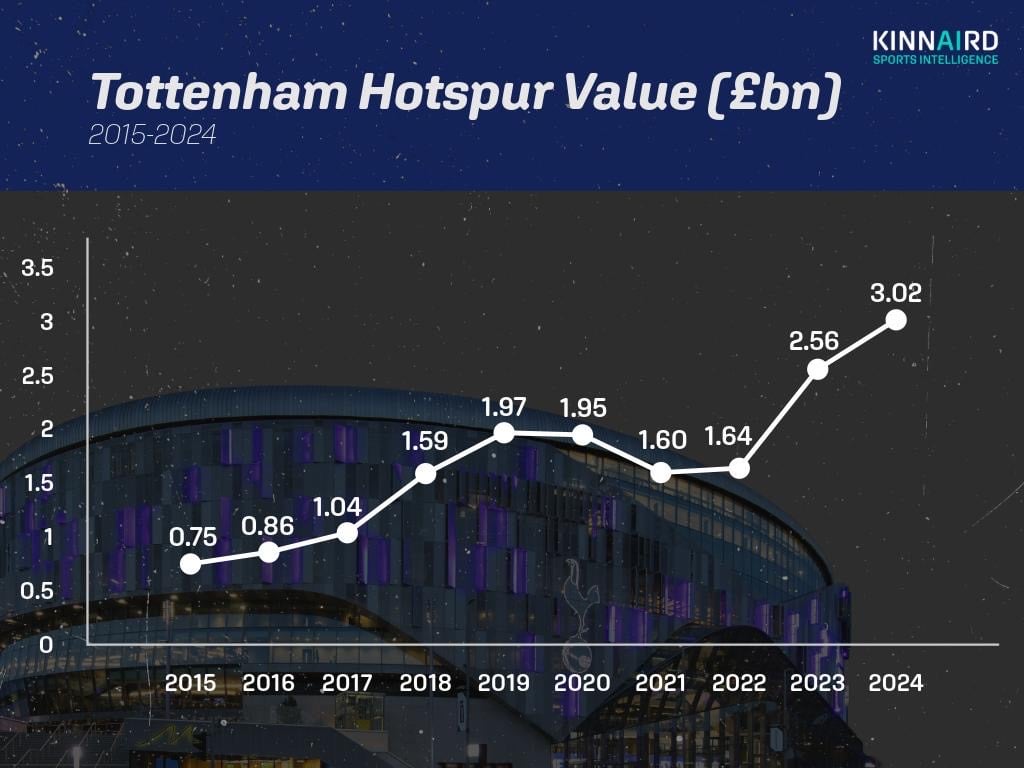

However, data-driven financial insights platform Kinnaird Sports Intelligence has pegged Spurs at the top-end of that range and as the second-most valuable club in the Premier League, behind only Man City.

Significantly, their Valuation Model emphasises inherent, underlying value as opposed to indexing against recent transactions and uses a scientific formula to arrive at a specific number.

“Tottenham represent one of the Premier League’s most impressive commercial transformations,” says Kinnaird’s founder Joe Roberts, speaking exclusively to TBR Football.

“They have leveraged their multi-purpose stadium – valued at £1.5 billion as of June 2024 – to quadruple commercial revenue over the past decade, effectively decoupling commercial growth from sporting success.

“The Kinnaird Valuation Model, which heavily weights commercial revenue as an indicator of brand strength and resilience to sporting volatility, ranks Tottenham exceptionally well.

“The club’s latest accounts reveal Spurs generated nearly as much commercial revenue as they paid out in wages and salaries – delivering the Premier League’s highest brand strength multiplier.

“A stadium re-evaluation uplift and investment in the playing squad have also contributed to the sharp rise in valuation in recent years.

“We expect Champions League broadcasting revenue and increased stadium utilisation to consolidate the club’s position as a financial powerhouse in world football this season.”

Tottenham’s value over the years, according to Kinnaird

Per Kinnaird’s model, Spurs’ value has nearly quadrupled over the last decade.

The biggest driver, of course, has been the new stadium with its enormous matchday income and ancillary revenue benefits.

Crucially, the Tottenham Hotspur Stadium has delivered what finance heads call ‘good-quality earnings’, i.e., revenue that doesn’t disappear if Spurs don’t qualify for Europe or go years without silverware.

Their Kinnaird Valuation Model KVM uses three-year averages of revenue, EBITDA [earnings before interest, depreciation and amortisation], wages, and commercial income to smooth out one-off spikes.

It excludes ‘soft’ loans from shareholders, adds a ‘squad value uplift’ for homegrown talent and player sale profits, and applies profitability and brand strength multipliers to arrive at its conclusion.

That is unlike traditional methods for valuing a club, which often focus solely on balance sheet valuations, comparable takeovers, or discounted cash flow analysis.

Minority investment ‘most likely’ for Spurs, says Kieran Maguire

TBR Football is aware of at least two parties besides the two consortia said to have submitted a bid that have also conducted due diligence with a view to a potential full takeover of Tottenham.

The mood music within the football finance industry meanwhile is that the Lewis family’s statement that the club is ‘not for sale’ should be taken with a lorry load of salt.

According to one expert, a Man United-style deal whereby ENIC hand over operational control in exchange for a significant minority equity sale remains the probable way forward for the North London club.

“I’m very sceptical about the not for sale comment,” Kieran Maguire, football finance lecturer at University of Liverpool, exclusively told TBR Football.

“You don’t have to have a ‘for sale’ sign outside your house, but if someone walks up to your front door, knocks and says they want to offer you twice the market value for it, you would end up selling it.

“That is the case with a significant number of clubs in the Premier League, including Spurs. It’s a never say never philosophy when it comes to M&A work.

“We have seen Man City sell off a minority stake to Silver Lake. That has shown it is part and parcel of modern day football economics. Given Spurs ability to generate very, very impressive EBITDA numbers, that could be attractive to a minority investor.

“Could we end up in a situation where ENIC want to get into a relationship similar to the Glazer family and Jim Ratcliffe’s at Man United? I think that’s the most likely.

“They might sell off 20-25 per cent but the buying party gets a control contract which gives them stewardship over the day-to-day operations of the club.

“That would mean ENIC get the best of both worlds. They wouldn’t be on the hook if decisions go wrong, but they are on the upside if Spurs flourish because the value of the club would increase and they could then sell their shares at a later date.”

Receive weekly football news and updates to your mailbox